Monthly Market Review – March 2021

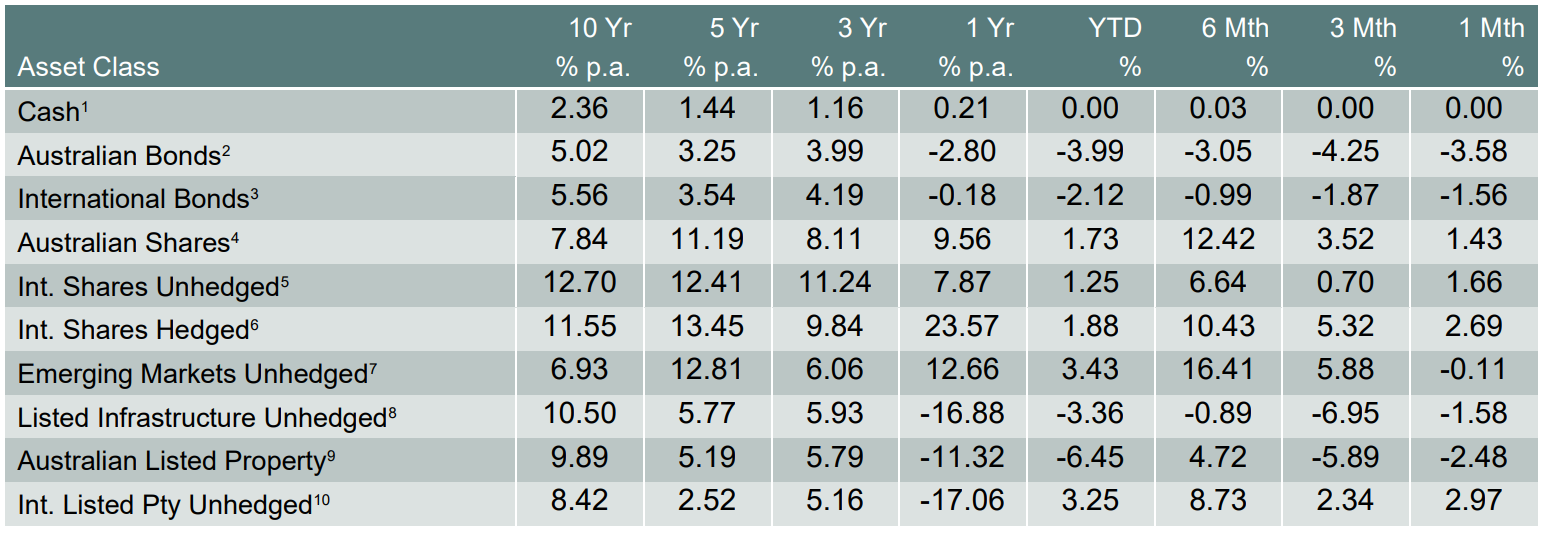

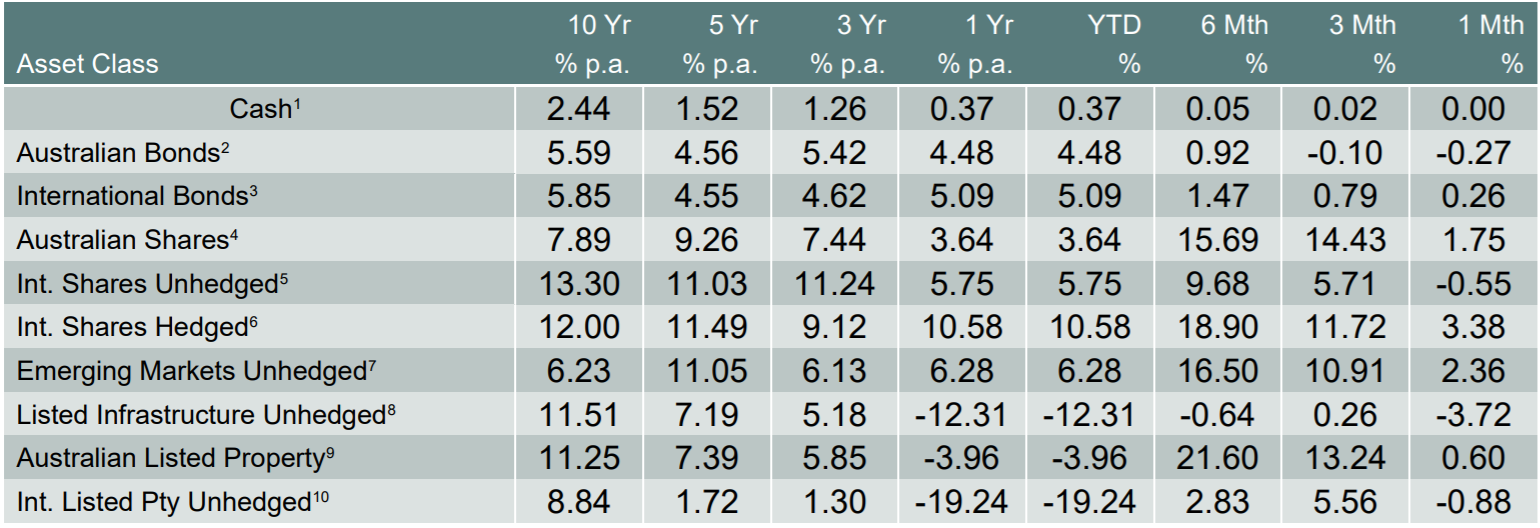

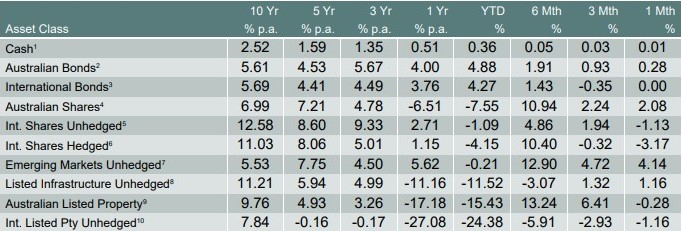

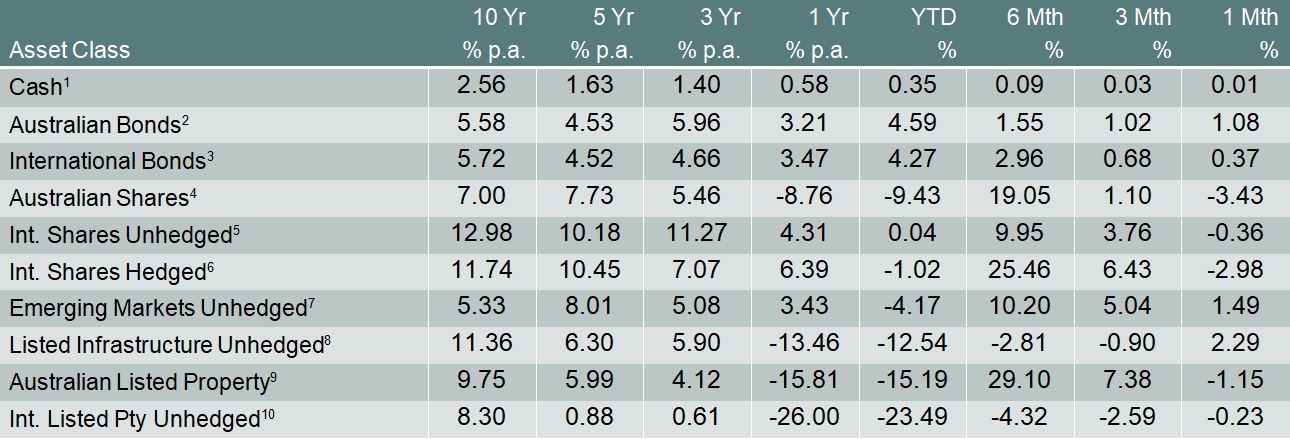

VIEW PDFHow the different asset classes have fared: (As at 31 March 2021)

1 Bloomberg AusBond Bank 0+Y TR AUD, 2 Bloomberg AusBond Composite 0+Y TR AUD, 3 Bloomberg Barclays Global Aggregate TR Hdg AUD, 4 S&P/ASX All Ordinaries TR, 5 Vanguard International Shares Index, 6 Vanguard Intl Shares Index Hdg AUD TR, 7 Vanguard Emerging Markets Shares Index, 8 FTSE Developed Core Infrastructure 50/50 NR AUD, 9 S&P/ASX 300 AREIT TR, 10 FTSE EPRA/NAREIT Global REITs NR AUD

Domestic and International Fixed Income

After rising sharply in February, US Treasury yields continued to edge higher in March, reflecting an improving outlook for the global economy due to the ongoing rollout of vaccines and the prospect of further significant fiscal stimulus in the US. At the end March, US President Biden announced a US$2.3 trillion “American Jobs Plan”. The plan focusses on infrastructure spending, spread over eight years, and is proposed to be funded by corporate tax increases spread over 15 years. This plan comes on top of a US$1.9 trillion relief package signed into law by President Biden in early March, and a US$900bn emergency relief package paid out in January.

The Biden administration is expected to announce another package in coming weeks focused on childcare, healthcare and education, which will be funded by tax increases on wealthy individuals. As a result of the huge fiscal packages proposed by the Biden administration, the market is expecting the US economy to recover strongly. The markets’ belief in economic recovery and the inflation that may result have been contributing factors to rising bond yields. However, Central banks remain dovish and have reiterated their commitment to keep easy monetary policy in place for an extended period.

After increasing sharply in February, Australian government bond yields declined slightly in March. Bond prices were supported after the RBA reiterated its commitment to its 3-year bond yield target of 0.1% and reinforced its message that they do not expect the cash rate to increase until 2024 at the earliest. In its March meeting press release, the RBA also flagged that they are “prepared to do more” bond purchases if deemed necessary.

Australian Equities

The S&P/ASX All Ordinaries Index rose by 1.8% in March, underperforming a 4% gain (foreign currency hedged) in international share markets. The best performing sectors for the month were consumer discretionary and utilities. The labour market recovered further in February, with a decrease in the unemployment rate to 5.8%. The Australian housing market also continued to rise in March, increasing by 2.8% according to CoreLogic, which is the fastest monthly increase since the late 1980s. Strength in the housing market has been driven by strong demand from first home buyers.

International Equities

International share markets (foreign currency hedged) rallied by 4% in March. Share markets were buoyed by an improving outlook for the global economy due to the ongoing rollout of vaccines, together with the prospect of further significant fiscal stimulus in the US.

The S&P500 rose by 4.4%, driven by strong gains in value-oriented stocks which are expected to benefit from a strong global economic recovery. By contrast, high multiple and long duration growth stocks, such as US technology stocks, underperformed shorter duration and more cyclically levered-value stocks over the month.

European shares rallied in March, while emerging market shares underperformed due to weakness in Chinese equities. Chinese equities were reportedly weighed down by concerns around earnings and tighter liquidity conditions from the People’s Bank of China.

Australian Dollar

The Australian dollar decreased modestly in March alongside a decline in iron ore prices (albeit from very high levels) and a narrowing in the spread between Australian and US government bond yields.

Disclaimer

The information contained in this material is current as at date of publication unless otherwise specified and is provided by ClearView Financial Advice Pty Ltd ABN 89 133 593 012, AFS Licence No. 331367 (ClearView) and Matrix Planning Solutions Limited ABN 45 087 470 200, AFS Licence No. 238 256 (Matrix). Any advice contained in this material is general advice only and has been prepared without taking account of any person’s objectives, financial situation or needs. Before acting on any such information, a person should consider its appropriateness, having regard to their objectives, financial situation and needs. In preparing this material, ClearView and Matrix have relied on publicly available information and sources believed to be reliable. Except as otherwise stated, the information has not been independently verified by ClearView or Matrix. While due care and attention has been exercised in the preparation of the material, ClearView and Matrix give no representation, warranty (express or implied) as to the accuracy, completeness or reliability of the information. The information in this document is also not intended to be a complete statement or summary of the industry, markets, securities or developments referred to in the material. Any opinions expressed in this material, including as to future matters, may be subject to change. Opinions as to future matters are predictive in nature and may be affected by inaccurate assumptions or by known or unknown risks and uncertainties and may differ materially from results ultimately achieved. Past performance is not an indicator of future performance.